The U.S. Defense Logistics Agency holds enough rare earth permanent magnet material to cover roughly two months of military demand at wartime burn rate, according to a March 2026 report attributed to the South China Morning Post and circulated through African and U.S. defense press. The Strategic Petroleum Reserve, for comparison, currently holds about 19 days of U.S. crude oil consumption or 47 days of net imports, depending on which side of the equation is counted.

Both numbers are imperfect. Both are also the same kind of number: a finite buffer against a country that no longer ships the way it used to. The petroleum buffer covers an entire economy. The rare earth buffer covers a defense industrial base.

What neither buffer covers, directly, is the part of the American economy that quietly built itself on the same chemistry as a guided missile motor. Every permanent-magnet electric vehicle traction motor on a U.S. road, from the Tesla Model 3 to the Ford Mustang Mach-E to the GM Ultium platform underpinning the Chevrolet Equinox EV, Cadillac Lyriq, and GMC Hummer EV, uses a neodymium-iron-boron magnet. That magnet contains one to three kilograms of neodymium-praseodymium alloy and between 50 and 200 grams of dysprosium per traction motor, according to Benchmark Mineral Intelligence. China currently produces roughly 70 percent of the world’s mined rare earths and processes about 90 percent of them, per U.S. Geological Survey data for 2024.

The Trump administration’s response to that math has accelerated quietly through the spring. The clearest single move came on April 19, when the U.S. Development Finance Corporation confirmed a $50 million equity injection into a rare earth project in Phalaborwa, South Africa, despite an active diplomatic rift between Washington and Pretoria. Two more projects, in Mozambique and Angola, have been added since February.

What the two-month number actually counts

The figure originated in reporting cited by the South China Morning Post in early March 2026 and circulated through African and Western defense outlets, including Business Insider Africa. It refers to the Defense Logistics Agency’s National Defense Stockpile, the federal reserve of strategic materials managed by the U.S. Department of War for use during national emergency. The number is an estimate of how long the stockpile would last under sustained military demand if Chinese exports of rare earth oxides and finished magnets were cut entirely.

It is not a measure of how long American factories could keep making cars, wind turbines, or smartphones. According to the U.S. Government Accountability Office, the U.S. imported more than 95 percent of the rare earths it consumed between 2019 and 2022. That figure has since dropped to roughly 67 to 80 percent through 2025, helped by MP Materials’ restart of the Mountain Pass mine in California and the qualification of domestically processed neodymium-praseodymium oxide by Energy Fuels in Utah. The civilian flow is not stockpiled. It is replenished month by month from imports.

What the two-month stockpile does signal is the Pentagon’s readiness window. The number entered public attention against a specific backdrop. U.S. strikes against Iran began on February 28, 2026, and the Pentagon burned through roughly $5.6 billion worth of munitions during the first two days of the operation, according to three U.S. officials cited by The Washington Post on March 9. By the most recent Pentagon disclosure on May 12, the total cost of Operation Epic Fury had climbed to about $29 billion, most of it in munitions. The same NdFeB chemistry that drives a permanent-magnet traction motor in a passenger EV also appears in the guidance systems of precision-guided munitions, according to U.S. Government Accountability Office assessments.

What an electric motor needs from China

More than 90 percent of electric vehicles built worldwide use a permanent-magnet synchronous motor, or PMSM, with a neodymium-iron-boron rotor magnet, according to Benchmark Mineral Intelligence data published in August 2025. Together with axial flux motor designs, that magnet chemistry accounted for about 86 percent of EV motor production in 2024. The choice is not aesthetic. Permanent-magnet motors hit peak efficiencies of 94 to 97 percent, against 85 to 91 percent for induction motors, which translates directly into more usable range from the same battery.

Each magnet contains roughly 30 percent rare earth content by weight, with neodymium making up the largest share. Dysprosium and terbium, two of the heavy rare earths, are added in smaller amounts to keep the magnet from demagnetizing at the high temperatures a traction motor sees during sustained climbs or repeated hard acceleration. Dysprosium oxide currently trades between $200 and $400 per kilogram, depending on grade. Neodymium-praseodymium oxide has moved between $50 and $150 per kilogram over the past five years.

EV traction motor demand for rare earths reached an estimated 37 kilotons in 2024 and is forecast to climb to about 43 kilotons in 2025, on a trajectory toward 270 kilotons of total rare earth oxide equivalent demand by 2035, with electric motors and wind turbines accounting for most of the growth. That demand is layered on top of the dozens of small NdFeB micromotors inside every modern vehicle, electric or not, that drive everything from window regulators to seat adjusters to audio speakers.

GLOBAL SHARE

The Trump administration’s Africa pivot

The most visible move came on April 19, when the U.S. Development Finance Corporation, working through investment firm TechMet, confirmed a $50 million equity investment in the Phalaborwa Rare Earths Project in northern Limpopo Province, South Africa. The project is being developed by London-listed Rainbow Rare Earths and is built around two enormous phosphogypsum dunes, roughly 35 million tons in total, that are the byproduct of decades of phosphate fertilizer production at the site. The chemistry has already done most of the work. Rainbow’s process extracts neodymium, praseodymium, dysprosium, and terbium directly from the waste piles, rather than from fresh ore.

Rainbow Rare Earths CEO George Bennett told the Associated Press, in coverage carried by PBS NewsHour on April 19, that the company expects to supply predominantly the U.S. market, and that American interest in the project is largely defense-driven. Construction of the processing facility is anticipated in early 2027, with first rare earth output planned for 2028. Operational life is estimated at 16 years. Independent analysis from Ecofin Agency puts the project’s likely peak output at around 1,850 tons per year of neodymium and praseodymium combined.

Phalaborwa is one of several. In February 2026, Secretary of State Marco Rubio convened a ministerial summit with seven African governments, including rare earth-producing countries. The U.S. Trade and Development Agency followed with a $1.8 million feasibility study for the Monte Muambe rare earths project in Mozambique. The DFC has also committed $3.4 million to Pensana’s Longonjo project in Angola, which is awaiting up to $160 million in financing from the U.S. Export-Import Bank for a mine capable of producing 20,000 tons per year of mixed rare earth carbonate. Botswana, the third country named in March’s African and defense press coverage, hosts the Gcwihaba skarn project under Toronto-listed Tsodilo Resources, which confirmed in March 2026 that drill cores at the site contained all 15 rare earth elements on the U.S. 2025 Critical Minerals List.

What Tesla, Ford, and GM have said about it

At Tesla’s 2023 Investor Day on March 1, Colin Campbell, the company’s then-Vice President of Powertrain Engineering, told investors that Tesla’s next-generation drive unit would use a permanent magnet motor with no rare earth elements. “We have designed our next drive unit, which uses a permanent magnet motor, to not use any rare earth materials at all,” Campbell said. Tesla also disclosed at the same event that the Model 3 powertrain had already reduced rare earth content by roughly 25 percent since 2017. Campbell left Tesla in August 2023 to become CTO of battery-recycling firm Redwood Materials.

The next-generation rare earth-free motor has not yet entered production as of mid-May 2026. The Model 3, Model Y, Cybertruck, Model S, and Model X currently on dealer lots all rely on at least one permanent-magnet traction motor with NdFeB content, with the specific configuration varying by trim and drive layout.

Ford has not publicly disclosed a comparable rare earth-free traction motor program. The Mustang Mach-E and F-150 Lightning both use permanent-magnet motors. General Motors’ Ultium platform, which underpins the Chevrolet Equinox EV, Cadillac Lyriq, Cadillac Escalade IQ, GMC Hummer EV, and Chevrolet Silverado EV, also uses permanent-magnet traction motors with NdFeB rotor magnets. GM signed a long-term supply agreement with MP Materials in December 2021 to source U.S.-mined and U.S.-processed rare earth alloy and finished magnets for those motors, with a gradual ramp that began in 2023.

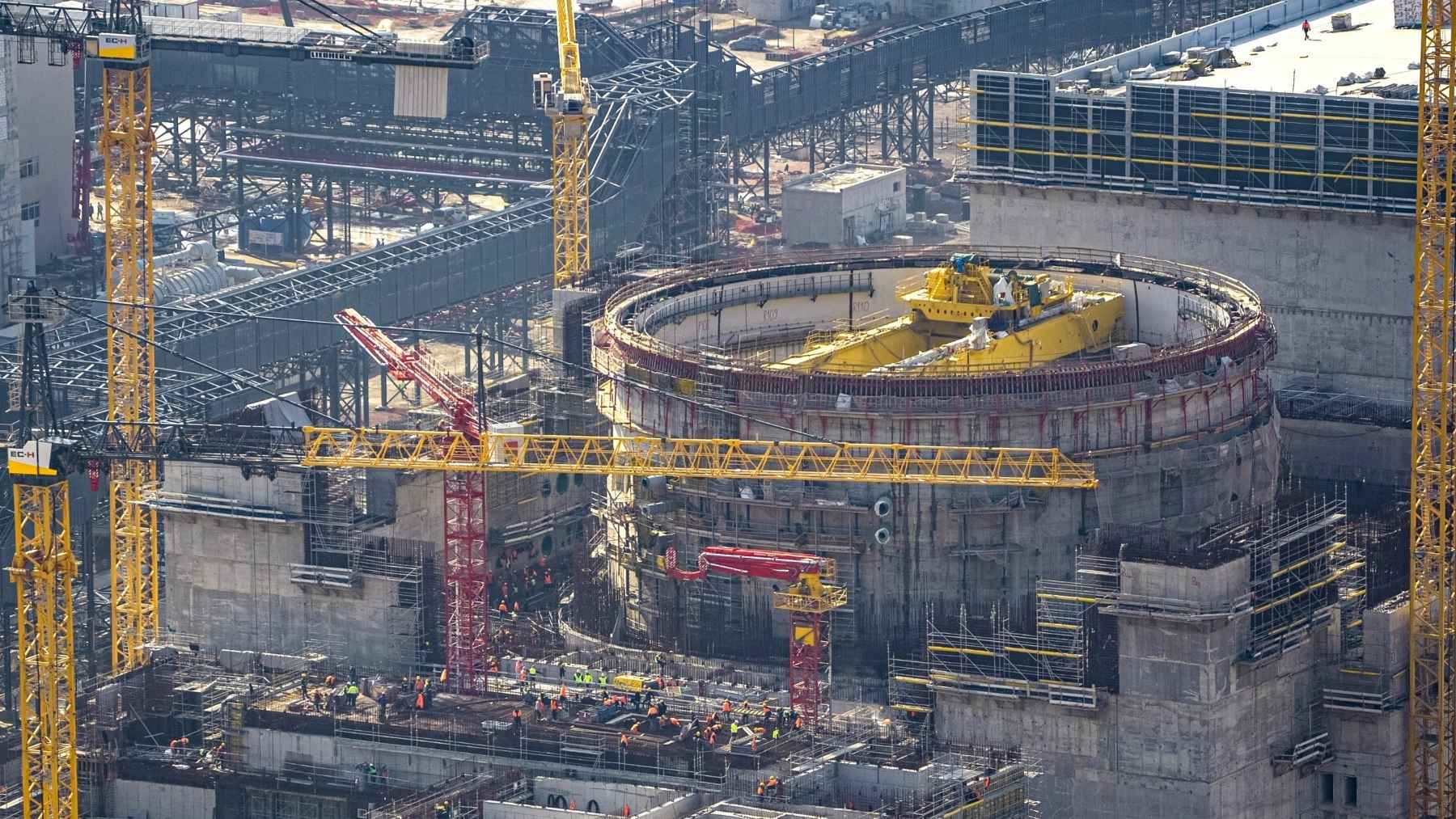

The Pentagon, for its part, took a more direct position in July 2025. The U.S. Department of War executed a $400 million preferred equity investment in MP Materials, along with a $150 million loan and a $110-per-kilogram price floor on neodymium-praseodymium oxide, making the federal government MP’s largest single equity holder. On February 26, 2026, MP announced it had selected a 120-acre site in Northlake, Texas, for “10X,” a $1.25 billion magnet manufacturing campus targeting roughly 10,000 metric tons per year of NdFeB magnet capacity by the end of the decade. The existing MP Materials Independence facility in Fort Worth, fewer than 10 miles south of the Northlake site, has been in commercial production since 2024 and currently runs at about 1,000 tons per year, with a 2,000-ton expansion underway.

The math that has not changed yet

Phalaborwa is scheduled to start extracting rare earths in 2028. Monte Muambe is still a feasibility study. Pensana Longonjo is targeting 2027 for first production. Tsodilo’s drilling campaign at Gcwihaba is set for 15,000 meters in 2026, with a maiden resource estimate to follow. The U.S. domestic magnet capacity under construction, between MP Materials’ Independence facility in Texas, the planned 10X campus in Northlake, and ReElement Technologies’ separation operation in Fishers, Indiana, is years from displacing imports at scale. The International Energy Agency’s most recent Critical Minerals Outlook projects China retaining its 90 percent share of separation capacity well into the 2030s under current trajectories.

None of which directly limits an American driver’s access to a new Equinox EV or Mach-E in 2026. The current supply chain is still flowing. The civilian inventory is still being replenished. What has changed, over the ten weeks since the original two-month figure first surfaced, is the political price of leaving it unchanged. The Phalaborwa investment closed despite a presidential executive order from February that froze most other financial assistance to South Africa. The Rubio summit gathered seven African mineral economies in the same room. The Pentagon took the largest single equity position in the only fully integrated U.S. rare earth magnet producer.

Two months is the number that did the political work. Whether it holds up under audit, whether the actual stockpile is closer to ninety days or thirty, is something the Defense Logistics Agency does not publish at the line-item level. What it has confirmed is that it is buying more.