While the United States has seen vehicle prices rise over the last year, one car-related expense is slowly declining. Starting in 2025, car insurance rates started to drop — well, depending on where you live.

According to insurance broker Insurify, the average annual full-coverage premium fell in 2025 by a whole 6%. Hey, we’ll take it. After analyzing over 197 million rates from drivers throughout the United States, Insurify found the average to be $2,144. However, only some states helped drop the rate.

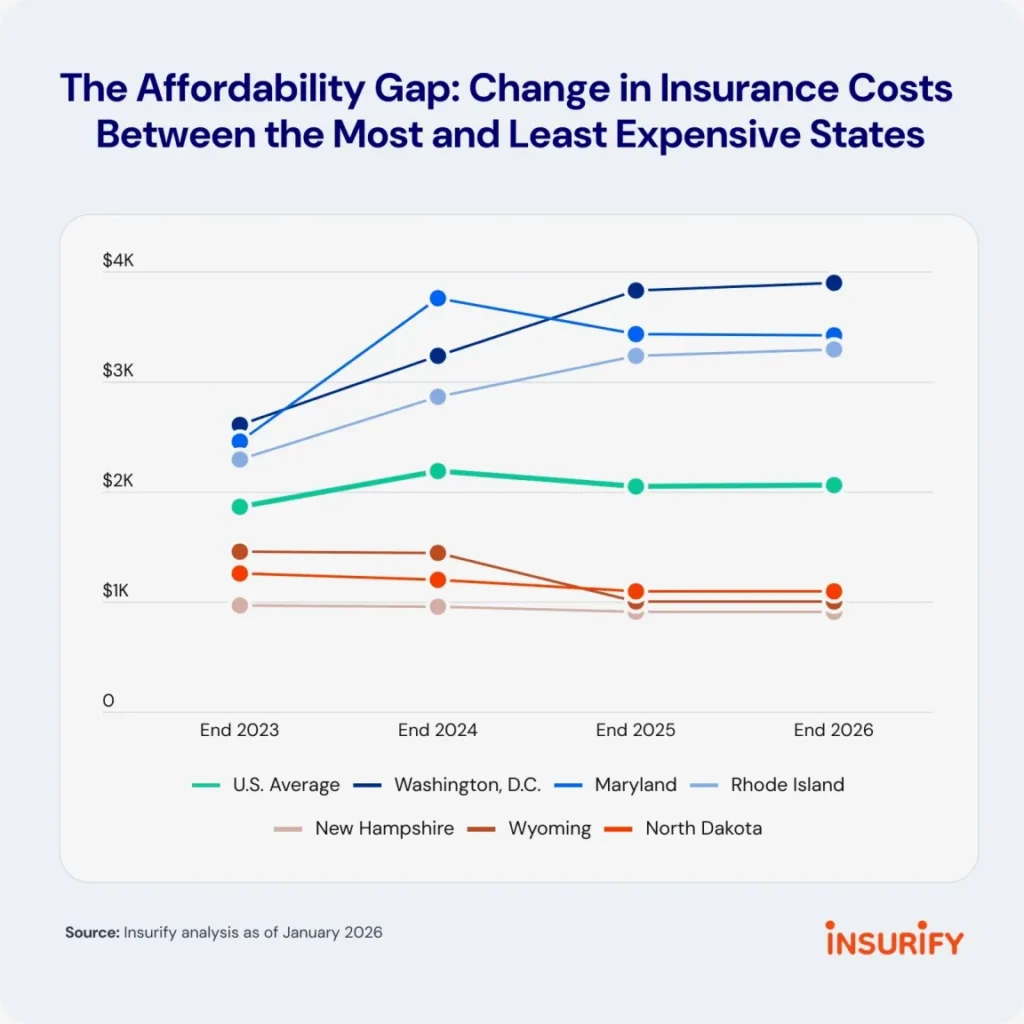

Thirty-nine out of 50 states saw a decrease in their insurance premiums. Most decreases were not dramatic, but some standouts include Arkansas, Iowa, and Wyoming’s 20% cuts. On the other hand, rates went 12% up in Michigan, 13% in Rhode Island, 18% in Washington D.C., and a whopping 20% in New Jersey. The state with the highest car insurance is Washington D.C., which has skyrocketed to $4,017.

Insurify Senior Carrier Partnerships Manager Daniel Lucas said: “D.C. lends itself to high car insurance costs on multiple fronts. It’s a highly congested, high-cost-of-living city with dangerous driving habits. Given the high financial risks insurers face, there’s little incentive, and little margin, for companies to cut premiums.” If that’s the case, where’s Florida sitting on the list?

If you live in one of the cheaper states — rejoice! Insurify claims the decline will continue into 2026. If you’re driving a Tesla, however, don’t count yourself lucky just yet. Insurify found that the Tesla Model X saw a 7% increase, while the Tesla Model S saw a 9% increase. The other 48 popular models from the survey saw price cuts. It’s not a good time to be a Tesla owner if you are looking to make or save money.

Why are insurance rates decreasing?

It seems a bit too good to be true, in all honesty. The average price of a new car in the United States has continued to climb up and up and up, now sitting at $50,000. At this point, most new cars are purchased by those who make well over six figures. We have Ford promising a $30,000 electric pickup, but the country seems to be floundering quite a bit due to the ongoing 15% import tariffs on cars and materials and continued pressure from China and its cheap-o EVs.

So, with the current state of the economy, how is insurance suddenly going down after a 46% increase from 2022 to 2024? According to Insurify, insurance companies began charging more after 2020 due to increased risky driving during the pandemic and higher repair costs when those vehicles were full of new, pricey tech. I went to research this since it sounded sorta like baloney since fewer people were on the road during COVID-19, but the AAA actually found that dangerous behaviors like speeding, not using seatbelts, and driving under the influence of alcohol “significantly” increased compared to pre-pandemic times. Was it a “we’re all gonna die anyway” attitude? Maybe drivers getting sloppy with fewer people on the road to worry about? Either way, 14,528 people were killed in crashes on the United States roads from 2020 to 2022, a 17% increase in traffic-related deaths.

There is a reason we try to forget this time, alright? With the pandemic further behind us and drivers returning to a normal level of drinking and driving, it seems insurance companies haven’t felt the need to dramatically increase premiums in advance. Oh, and it also helps that insurers have accumulated tons of money from those increased premiums, which has helped them feel less impacted by tariff-related price hikes over the last year, like increased repair costs, writes Insurify. Ah, thanks for taking enough of our money to feel secure in these times! But as tariffs continue to affect all industries, insurance companies are trying to lower their prices — even a little — to attract new customers. Anything to give them a bit more moolah during these tough times. And by tough times, I mean a lack of lunatics speeding without seatbelts to justify major premium hikes.

The reasons for the decrease in insurance premium rates may not be the most pleasant to hear, but a win is a win at this point. And I’ll take that 6% savings.